AI Validation Is the New Audit Evidence Risk

As discussed in our prior articles, What Regulators Expect to See When AI is Used and AI Governance Belongs in the Boardroom, Not the Server Room, firms increasingly recognize that AI governance belongs within the system of quality management. However, inspection experience shows that even well-designed governance frameworks do not eliminate risk. Significant failures occur not only at the policy level, but also at the engagement level, where AI outputs are relied upon as audit evidence without sufficient validation.

This article focuses on that execution gap. Specifically, it examines why validation of AI is emerging as one of the most significant audit evidence risks facing public company auditors today.

For public company auditors, AI validation is no longer a technical exercise. It is an audit quality issue — and increasingly, an inspection issue. In the eyes of regulators, AI does not reduce evidentiary requirements; it changes how evidence must be evaluated, corroborated, and defended

.How AI Changes Audit Evidence—and Raises the Validation Stakes

PCAOB auditing standards governing audit evidence have not been rewritten for AI. The fundamental requirement remains the same: auditors must obtain sufficient appropriate audit evidence to support their opinion. What has changed is the evidence pipeline: when AI is used, outputs are often indirect (generated through models rather than procedures alone), abstracted (summaries, risk flags, or scores rather than raw data), and less intuitive to evaluate using traditional audit instincts.

This creates a new risk: auditors may rely on AI assisted outputs without fully validating how those outputs were produced, what they mean, or whether they are reliable.

From an inspection perspective, AI introduces a simple but critical question: How does the auditor know the AI result is reliable enough to rely on as audit evidence? Inspectors are increasingly focused on whether the engagement team can demonstrate the completeness and accuracy of inputs, the reasonableness of assumptions/logic (including prompts), the consistency and explainability of outputs, and the auditor’s independent evaluation and corroboration. A common misconception is equating firm tool approval (vendor diligence, IT review, or risk assessment) with audit evidence validation. Approval is necessary, but it is not sufficient: validation must occur at the engagement level, in the context of the specific audit objectives, data, and risks.

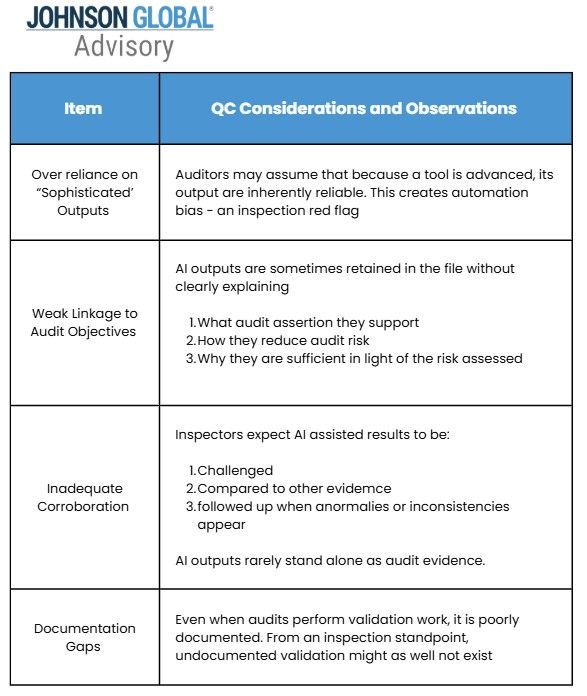

Where AI Validation Commonly Breaks Down

In practice, AI validation risk often arises in predictable ways:

AI Validation Is Becoming a Quality Control Issue

A common misconception is equating firm-level approval of an AI tool with audit evidence validation. Governance determines whether a tool may be used within the firm. Validation determines whether the results produced by that tool can be relied upon as audit evidence in a specific engagement.

Even when AI use is properly governed, inspection risk arises at the engagement level if auditors cannot demonstrate how inputs were evaluated, how assumptions or parameters were understood, and how outputs were independently assessed and corroborated. In these situations, the existence of policies or tool approvals does not mitigate inspection risk.

Under PCAOB standards, engagement teams and engagement partners are responsible for the sufficiency and appropriateness of audit evidence, regardless of how that evidence is generated. If validation work is unclear, undocumented, or unsupported, inspectors will not accept “the system did it” as a defense. AI validation, therefore, cannot be fully delegated to the National Office, IT, data teams, or innovation groups. Engagement teams must be able to explain and defend their reliance on AI outputs within the context of the specific audit objectives and risks.

When similar validation weaknesses recur across engagements, inspectors may view the issue as a firm-level quality control matter rather than an isolated engagement deficiency. However, those weaknesses are typically identified through engagement-level audit evidence findings, where reliance on AI cannot be supported by sufficient documentation and professional judgement.

From an inspection standpoint, firms are increasingly expected to demonstrate, through engagement execution and documentation:

- Governance and formal approval processes for AI tools

- Alignment of the AI to the audit objectives

- Assessment of reliability of inputs and validation of outputs

- Robust supervision and engagement partner involvement

- Evidence of professional skepticism throughout the AI audit procedures

- Inspection ready documentation explaining why AI was used and how results were evaluated

What Audit Leaders Need to Know

AI Is reshaping what “Sufficient Appropriate Audit Evidence” Really Means. Validating AI in an audit context applies to both inputs and outputs—and the connection between them. Focusing only on outputs is insufficient and leaves firms inspection vulnerable. Takeaways for firms using (or planning to use) AI include:

- Start with the audit objective, not the tool. Define the assertion(s), risk, and decision the AI output will support—and what “good evidence” looks like for that use case.

- Validate inputs, logic, and outputs—then document it. Be prepared to show completeness/accuracy of data, how prompts/parameters were designed and controlled, and how results were evaluated and corroborated.

- Do not confuse tool approval with engagement-level validation. Even if an AI tool is firm-approved, the engagement team still needs evidence that it performed reliably for this client, this data, and this risk.

- Design procedures that remain inspection-ready. Ensure you can explain “why AI,” how exceptions were addressed, and how professional skepticism was applied—without relying on “the system did it.”

- Clarify ownership and escalation. Assign who performs validation, who reviews it, and when results require escalation to specialists, the engagement partner, or the National Office.

- Build repeatability into your approach. Standardize workpapers, testing steps, and acceptance criteria, so validation is consistent across engagements and defensible under inspection.

Many of the considerations outlined above will feel familiar to audit leaders who have already grappled with governing traditional software‑based audit tools. In fact, these takeaways closely align with the control environment principles discussed in our prior JGA article, “Software Audit Tools: Designing and Implementing the Control Environment.” AI does not replace those foundational expectations—it amplifies them, raising the stakes for governance, oversight, and audit quality execution.

JGA Final Thoughts

AI raises the evidence bar, not lowers it. AI validation in auditing is about demonstrating that reliable outputs were produced because reliable inputs were processed appropriately for the intended audit purpose. If either side fails, the audit evidence fails.

AI has the potential to strengthen audits—but only when validation occurs with the same rigor applied to any other form of audit evidence. AI validation is rapidly becoming the new audit evidence risk—and firms that fail to treat it as such will feel it first in PCAOB inspections.

Need help validating your AI tools? Contact your JGA audit quality expert to schedule a consultation and assess whether your firm’s reliance on AI is supportable.