Navigating AI Governance: JGA Authors Governance & Compliance Chapter of the Accounting AI Playbook

This is an exert of the AI Accounting Playbook.

Building Trust in AI Accounting

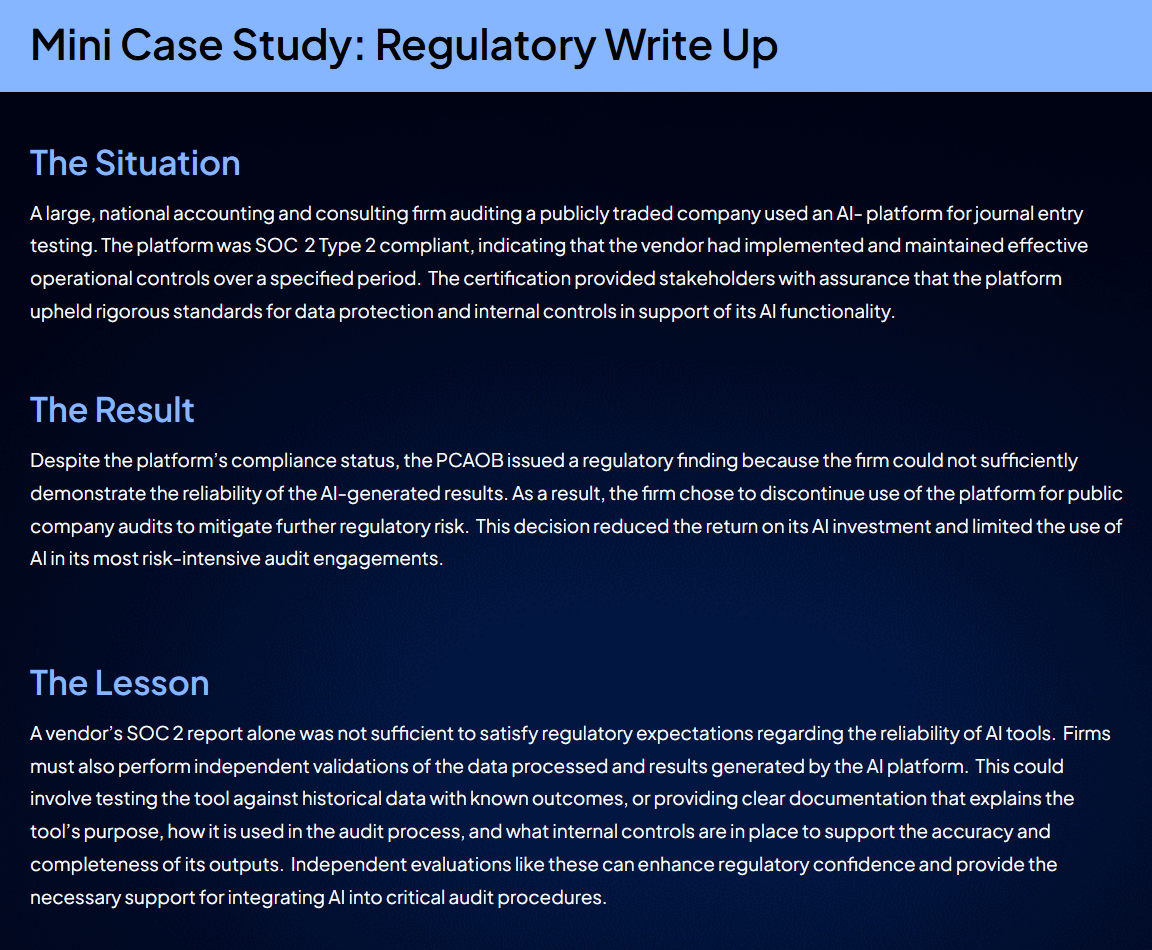

As accounting firms adopt AI tools in audits, they face new questions about reliability, transparency, and compliance. Regulators like the PCAOB have made clear that if AI outputs can’t be explained or reproduced, they could violate existing standards. Yet formal guidance on AI use in audits remains limited, leaving firms unsure about how to move forward.

Some firms have responded by limiting AI to non-public clients, but this caution also presents a chance to lead. Firms that build strong AI governance practices now can stay ahead of future regulation and establish trust in their use of AI. This chapter covers key compliance barriers, governance best practices, and steps to create a trusted control environment.

Key Compliance Barriers

Accountants face several key compliance barriers when using AI, particularly as regulators such as the PCAOB, AICPA, and SEC increase their scrutiny.

Explainability

One major challenge is explainability. Many AI models, especially machine learning and generative AI, don’t clearly show how they reach conclusions. This is a problem for auditors who need to support their findings.

This lack of clarity makes it harder to meet audit evidence requirements, which must be sufficient, appropriate, and easy to understand, as outlined in PCAOB standard AS 1105.

Poor Documentation

Poor documentation is another major issue. This includes inadequate records of data inputs and outputs, training data, model logic, and controls over changes.

Such deficiencies may violate documentation and risk assessment requirements, as seen when audit teams use AI for journal entry testing without documenting the rationale for flagged entries or threshold settings.

Data Privacy

Data privacy becomes a concern as firms use AI to handle large amounts of sensitive financial and personal information. This can lead to violations of laws like GDPR and CCPA, especially when client data is processed in cloud or third-party systems.

Firms often struggle to maintain consistent policies for data classification, encryption, and access. Auditor independence may also be at risk if AI tools are built by a firm’s advisory armor are deeply integrated with a client’s systems. For instance, if both the firm and client use the same predictive AI tool for forecasting, it could lead to a self-review threat.

AI Skills Gap

A skills gap and overreliance on AI further complicate compliance. Many auditors lack the training needed to critically evaluate AI outputs or to recognize when human judgment should override algorithmic conclusions.

This can lead to audit failures, such as misinterpreting a false negative from an AI-driven risk assessment as a clean result.

Validation and Testing

Testing and validating AI tools is another challenge, especially for tools that keep learning over time. Firms need to test tools when they’re first used and then on a regular basis, just like they do when relying on third-party service providers.

But this is hard to do if the AI vendor doesn’t offer enough detail about how the tool works or the controls in place.

Change Management

Managing updates and changes to AI models is a concern. If a tool is updated or retrained without documentation, it can lead to inconsistent results.

For example, a model may flag different transactions in different quarters without any clear reason why. Many firms also lack a formal AI governance plan tied to their quality management systems, which causes inconsistent control practices and unclear responsibilities.

Lack of Guidance

Regulators have been slow to issue formal guidance on how AI should be integrated into the audit process, leaving many firms in a state of uncertainty.

The good news is that momentum is building. PCAOB Board Member Christina Ho has publicly emphasized the transformative potential of AI in auditing, particularly in automating routine tasks such as cross-referencing data, extracting key contract terms, and documenting interviews. She has advocated for the PCAOB to evolve its standards to promote responsible AI use, calling for transparency, bias mitigation, and auditability in AI tools.

Similarly, the International Auditing and Assurance Standards Board (IAASB) has demonstrated its commitment to supporting firms by releasing its Technology Position, which is a strategic framework that outlines how the board will adapt auditing standards to align with emerging technologies, including AI.

Until these guardrails are firmly in place, firms should proactively develop internal AI frameworks modeled on established control standards. COBIT can support firms in assessing and governing AI systems, including data and system integrity. COSO can be applied to evaluate AI governance, model risk, and internal control implications, particularly when AI impacts financial reporting or ICFR. NIST provides guidance to help firms build trustworthy AI systems and establish appropriate cyber security and governance protocols.

Best Practices for Governance

To use AI confidently and compliantly in accounting, especially in regulated environments like audit and assurance, firms should implement strong governance practices that align with both regulatory expectations and ethical standards.

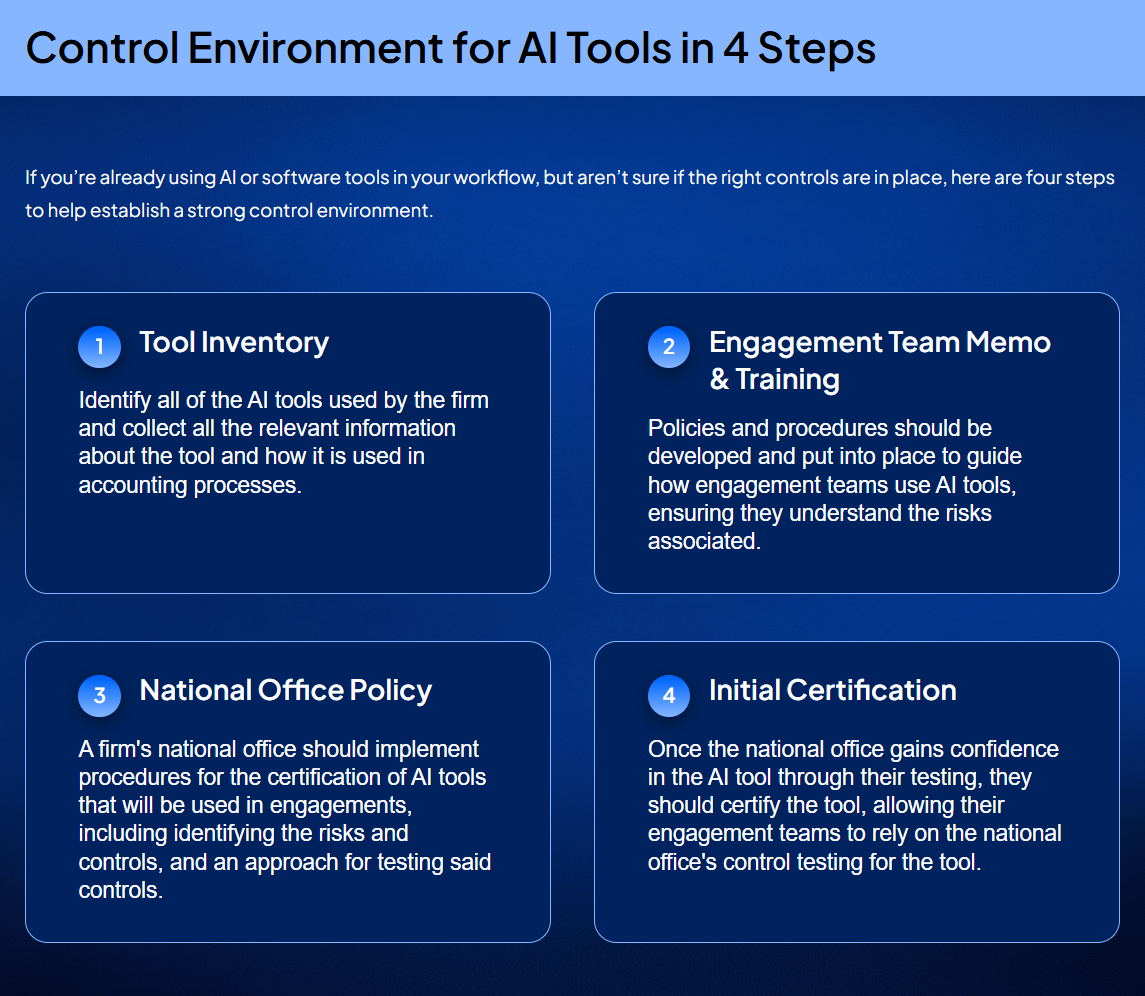

1. Test AI Internally Before Use In Engagements

Before you bring AI into your audits, you’ll need to put it through its paces. The starting point is an internal review and certification process, ideally led by your firm’s risk or national office. They should evaluate the AI tool’s design, logic, and controls, and may require your vendor to share documentation, control reports, and allow independent testing.

A great way to do this is by running the AI on historical data from past audits with known results. That helps confirm whether the AI delivers the same conclusions auditors already reached.

Scenario analysis is another smart move. Challenge the AI with tricky edge cases like known fraud or anomalies. This can expose blind spots or bias in the model.

Be sure to maintain a complete audit trail of how the tool was tested and what controls were in place. If any issues pop up during testing, document and resolve them.

And before you roll it out firm-wide, get an independent review of the tool. Think of it like a second set of eyes, similar to a concurring partner review. Only once your firm is fully confident in the tool should it be used in your accounting processes.

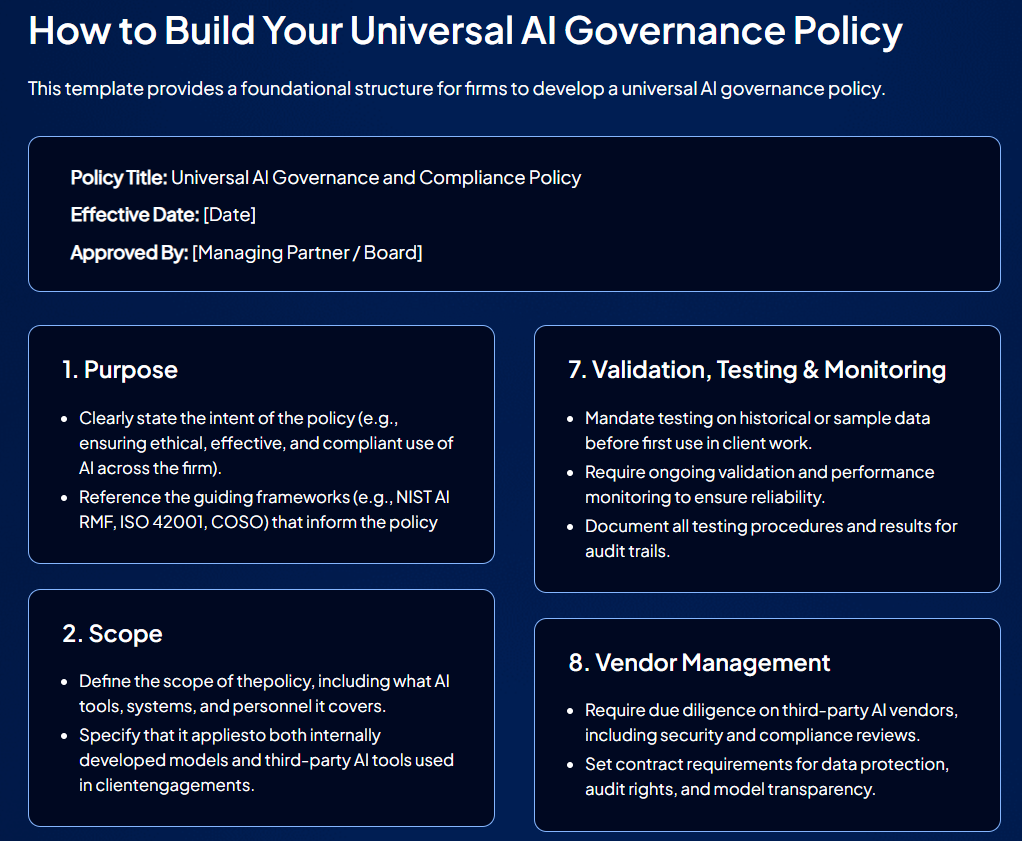

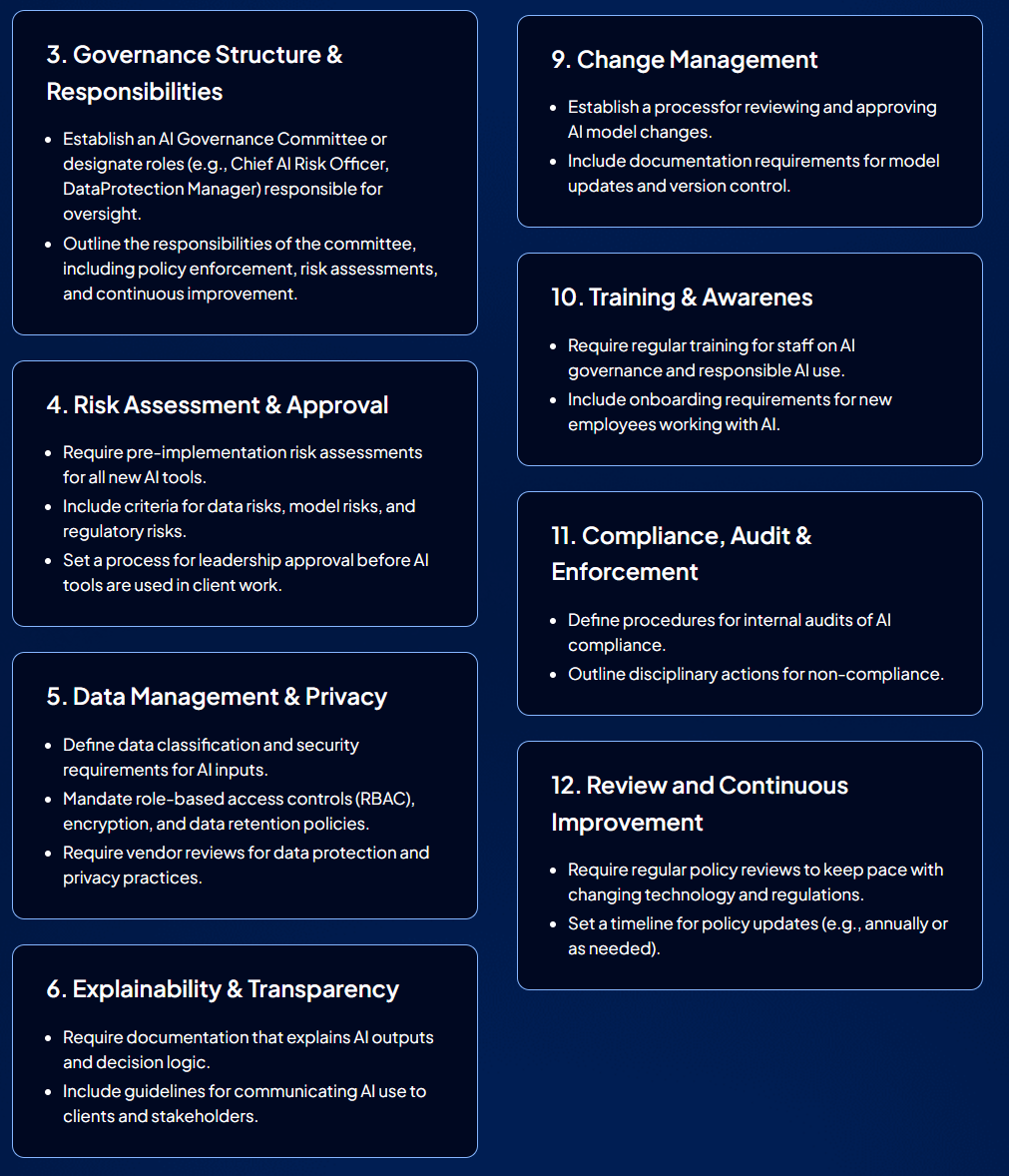

2. Develop AI Governance Policies

Strong policies lay the foundation for responsible AI use. These should outline your standards for data inputs, risk reviews, decision-making responsibilities, and transparency.

Deloitte recommends a universal governance policy that applies to all AI technologies across the firm. This policy should define acceptable (and prohibited) use cases, require approval for new AI tools, and establish review intervals.

Ethical usage also needs to be a priority. That means clear guidelines around privacy, bias, and legal compliance — with transparency as a core value. Internally and externally, stakeholders should understand when and how AI is being used in order to build trust in AI usage.

To oversee this, consider forming a dedicated AI GRC (Governance, Risk, Compliance) team. Roles might include a Chief AI Risk Officer, Data Protection Manager, AI Project Manager, and an AI Governance Committee.

Need help building your framework? Look to proven models like NIST AI RMF and ISO 42001. COSO’s recent guide Realize the Full Potential of AI shows how to extend COSO’s ERM framework to AI, and it’s a great place to start.

3. Implement Data Quality Controls

AI tools are only as reliable as the data they process. The old adage “garbage in, garbage out” underscores the importance of data quality in AI-driven accounting. To minimize the risk of inaccurate or biased AI outputs, firms should implement data validation, cleansing, and standardization processes. High-quality data improves AI performance and supports more reliable audit conclusions.

Protecting sensitive data is also crucial. Firms should limit access to confidential information using role-based access controls (RBAC) and multi-factor authentication (MFA). Audit logs tracking data access provide an added layer of oversight, helping firms monitor and secure critical information.

Data lifecycle management is equally important. Retention and deletion policies should be in place to ensure outdated data does not become a liability. While GDPR is an EU regulation, it sets a high standard for data management and serves as a strong benchmark for firms looking to enhance their data governance practices

AI Governance and Compliance Checklist

Use this checklist to guide your firm’s efforts in implementing sound AI governance and compliance practices.

Governance & Oversight

- Have you designated an AI Governance Officer or committee to oversee AI tools and compliance?

- Is there a formal AI governance policy that aligns with industry standards like NIST, COSO, and ISO?

- Are AI use cases approved by firm leadership before deployment?

AI Inventory & Documentation

- Have you created and maintained a complete inventory of all AI tools in use, including purpose, data sources, and vendor details?

- Is there a process for documenting model logic, data inputs, outputs, and changes?

- Are your AI systems mapped to specific regulatory requirements (e.g., PCAOB, SEC, AICPA)?

Explainability & Transparency

- Can your AI tools provide clear, explainable outputs that meet audit evidence standards?

- Are you documenting how AI tools reach their conclusions to support audit transparency?

- Are engagement teams aware of the limitations and appropriate uses of AI tools?

Data Privacy & Security

- Are data inputs for AI tools classified by sensitivity and protected by strong access controls?

- Have you implemented encryption, role-based access (RBAC), and audit logs for AI data?

- Are vendor data protection practices verified before use in client engagements?

Bias & Fairness Checks

- Are you regularly testing AI tools for bias or unfair outcomes?

- Are you adjusting models or their use if bias is detected?

- Are you following emerging best practices for bias mitigation and fairness in AI?

Validation & Testing

- Are AI tools tested on historical data before deployment?

- Are you performing scenario analyses with edge cases to identify potential weaknesses?

- Are you documenting all testing procedures and results for audit trails?

Change Management

- Is there a formal process for reviewing and approving AI model changes?

- Are you documenting all changes to AI models, including rationale and expected impact?

- Are engagement teams informed of significant AI model updates that could affect results?

Regulatory Alignment

- Have you mapped AI usage to relevant standards (e.g., PCAOB AS 1105, AICPA Code of Conduct)?

- Are you maintaining documentation to demonstrate AI compliance to regulators?

- Are you tracking regulatory developments to update your AI practices as needed?

Ongoing Training & Review

- Are staff regularly trained on AI governance policies and best practices?

- Are you conducting periodic reviews of AI use and compliance?

- Are you updating your governance approach as AI technology and regulations evolve?

This checklist can be incorporated into your firm's quality control program, supporting the responsible use of AI tools and alignment with U.S. regulatory expectations.

Chapter Summary

As AI becomes more integrated into accounting, firms must navigate regulatory complexities to ensure compliance and reliability. This chapter delves into key governance challenges, including regulatory uncertainty, explainability, and data privacy risks. It outlines best practices for AI implementation, such as internal testing, developing governance policies, and implementing data quality controls. Through a real-world case study and structured methodology for building a control environment for AI tools, readers will gain a comprehensive roadmap for establishing a compliant AI framework that fosters trust and strengthens audit integrity.

This is an exert of the AI Accounting Playbook.

About Johnson Global Advisory

Johnson Global partners with leadership of public accounting firms, driving change to achieve the highest level of audit quality. Led by former PCAOB and SEC staff, JGA professionals are passionate and practical in their support to firms in their audit quality journey. We accelerate the opportunities to improve quality through policies, practices, and controls throughout the firm. This innovative approach harnesses technology to transform audit quality. Our team is designed to maintain a close pulse on regulatory environments around the world and incorporate solutions which navigate those standards. JGA is committed to helping the profession in amplifying quality worldwide.

Visit www.johnson-global.com to learn more about Johnson Global.